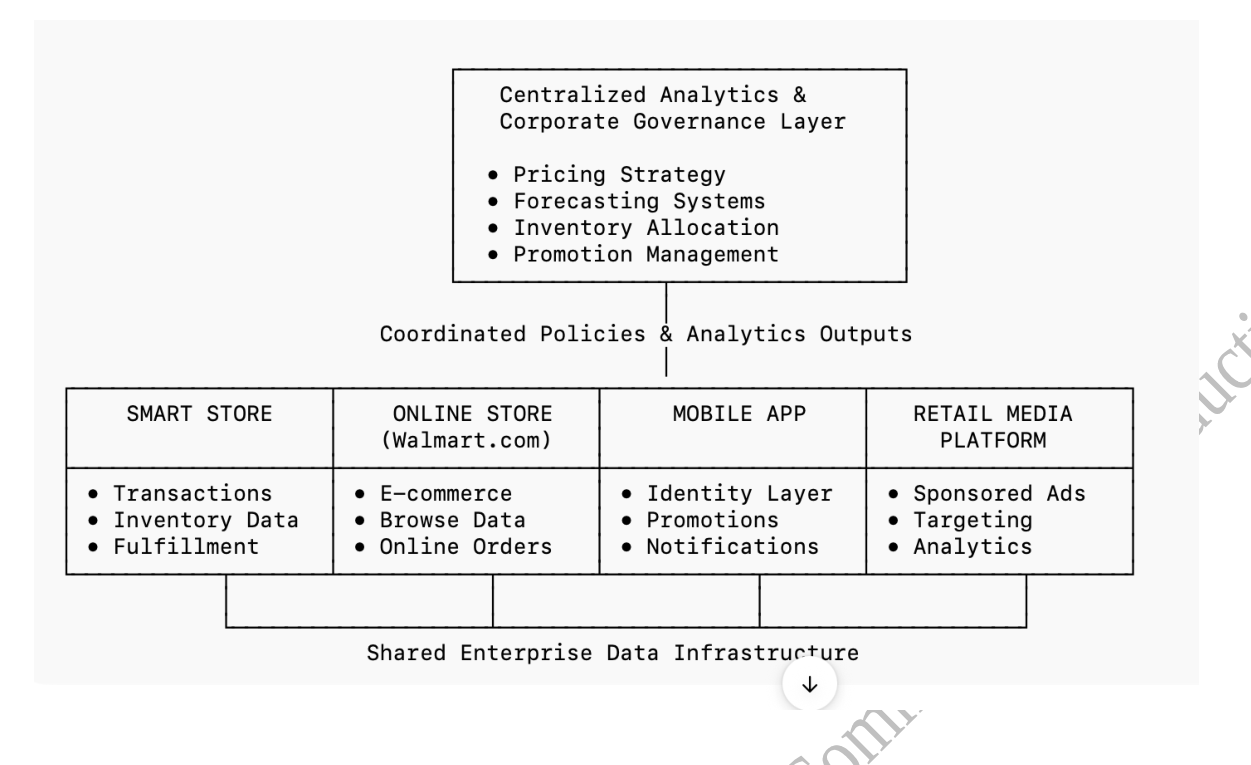

Walmart’s omnichannel architecture solves the same problem as KFC China’s super-app — but with a fundamentally different stack and a different theory of where value accrues. This case shows how the Customer Data Platform, Algorithmic Decision Center, retail-media network, and smart-store integration compose a U.S.-specific answer to AI-era retail.

- →The CDP + ADC pair is the U.S. analog to China’s private-domain stack. Same job (turn behavior into decisions); different architecture.

- →Retail-media network is a quiet flywheel. Store traffic and online behavior become advertising inventory, which becomes revenue, which funds further data investment.

- →Smart products + smart stores integration is where physical-digital boundaries dissolve in U.S. retail — not as a concept but as a P&L line.

- →The Walmart architecture cannot be copied piecemeal. The combination is the moat, not any individual module.

Monday-morning move: For brands operating in both U.S. and China, pick which architecture to learn from. They are structurally incompatible; mixing them produces a hybrid that wins neither.

For decades, Walmart’s dominance rested on physical scale. Thousands of stores, vast distribution centers, sophisticated logistics networks, and disciplined cost management enabled the company to deliver “Everyday Low Prices” at unmatched breadth. Its competitive advantage was built not on software, but on infrastructure.

By the early to mid-2010s—particularly between 2014 and 2016—the rapid acceleration of e-commerce fundamentally reshaped retail competition. Digital-native firms demonstrated that scale could expand without proportional investment in real estate. Algorithms replaced aisles. Data replaced foot traffic. Cloud infrastructure replaced storefronts. Amazon’s expanding Prime ecosystem, faster fulfillment, and increasingly sophisticated personalization capabilities signaled that digital coordination—not physical footprint alone—was becoming the primary source of advantage. Customer relationships were shifting from episodic store visits to continuous digital interaction.

In this environment, the traditional strengths of brick-and-mortar retailers appeared increasingly vulnerable. Large store networks carried fixed costs. Physical inventory required labor and coordination. In-store experiences struggled to match the personalization and speed of digital platforms. It was during this period of intensifying digital competition that Walmart confronted a fundamental strategic question: Can physical scale become a digital advantage rather than a structural liability?

The challenge was not whether Walmart should participate in e-commerce—it had already invested in online operations. The deeper issue was structural: could the company reorganize its massive physical infrastructure into a coordinated, data-enabled system capable of competing with asset-light digital giants?

Beginning in the mid-2010s, Walmart responded with a series of strategic initiatives that went beyond launching new digital features. By 2015, the company had become one of the world’s largest corporate technology investors, spending more than $10.5 billion annually on hardware, software, and telecommunications (Retail Dive, 2015; Walmart Annual Report, 2016). It expanded Walmart Labs—later consolidated into Walmart Global Tech—to institutionalize internal engineering, data science, and machine learning capabilities. At the same time, Walmart pursued broader organizational and strategic shifts: it accelerated omnichannel integration, scaling Buy Online, Pick Up In-Store (BOPIS) and curbside services across its network; it acquired Jet.com in 2016 to strengthen e-commerce talent, marketplace capabilities, and urban customer reach; it reorganized leadership to prioritize digital coordination and platform development; it invested in supply chain automation, data infrastructure modernization, and centralized analytics platforms; and it expanded marketplace participation and third-party seller integration to broaden assortment without proportional inventory expansion.

Rather than abandoning its store network, Walmart pursued a different strategy: transforming stores from cost-intensive endpoints into digitally connected nodes within a broader retail intelligence architecture.

1. Rewiring the Store Network: From Physical Footprint to Digital Infrastructure

As e-commerce accelerated in the mid-2010s, Walmart recognized that digital competition required more than an online storefront. Its store network, supply chain, pricing logic, and customer data systems operated largely as parallel structures. To compete effectively, these elements had to be integrated into a coordinated operating architecture. The objective was not to replace physical retail, but to make it programmable—capable of responding to demand signals, pricing inputs, and customer behavior in real time.

Over time, Walmart deployed a series of interconnected digital initiatives spanning customer interfaces, store operations, logistics, and enterprise analytics. These investments collectively embedded data capture, algorithmic support, and cross-channel synchronization into core processes.

These initiatives were not isolated upgrades. Together, they altered how stores functioned within the enterprise. Customer-facing systems such as the mobile app and digital receipts linked physical transactions to persistent digital identities. Omnichannel services synchronized online orders with store-level inventory and execution workflows. Inventory sensing technologies improved visibility into stock conditions and replenishment needs. Centralized analytics increasingly informed pricing, demand forecasting, and allocation decisions. Supply chain automation enhanced fulfillment responsiveness.

Retail media layered monetization onto the data generated by both online and in-store transactions, allowing Walmart to offer brands targeted advertising placements across its website, app, and selected in-store digital screens based on first-party commerce data. Walmart+ further strengthens this architecture by anchoring customer identity and recurring engagement within a subscription framework, increasing purchase frequency while reinforcing cross-channel data continuity (Walmart Press Release, 2020).

Importantly, these capabilities were embedded within existing operations rather than layered on top of them. Pricing decisions, inventory allocation, and fulfillment routing were progressively supported by centralized data systems, even as managerial oversight remained intact.

| Walmart Initiative Cluster | Strategic Focus | Contribution to Retail Intelligence Architecture |

|---|---|---|

| Mobile App, Digital Receipts, Scan & Go | Identity integration & engagement continuity | Connects offline and online behavior into unified digital profiles |

| Walmart+ Membership Ecosystem | Identity continuity & recurring engagement | Anchors subscription-based participation, increases purchase frequency, and strengthens lifetime value across channels |

| Personalized Promotions & Recommendation Systems | Data-driven relevance & targeting | Enables scalable personalization across touchpoints |

| Buy Online, Pick Up In-Store (BOPIS) & Curbside Pickup | Omnichannel fulfillment coordination | Converts stores into distributed logistics nodes |

| RFID Tagging & Computer Vision Monitoring | Real-time inventory visibility | Enhances store-level sensing, stock accuracy, and replenishment responsiveness |

| Electronic Shelf Labels & AI Pricing Systems | Coordinated price optimization | Synchronizes merchandising and pricing logic across physical and digital channels |

| Self-Checkout & AI-Based Monitoring | Transaction automation & friction reduction | Improves speed while generating structured behavioral data |

| Robotics & Algorithmic Warehouse Routing | Fulfillment efficiency & cost control | Strengthens logistics precision, scalability, and cost discipline |

| Blockchain & IoT-Based Traceability | Supply chain transparency | Improves product safety, traceability, and data visibility |

| Walmart Global Tech & Proprietary ML Platforms | Enterprise analytics & model training | Centralizes forecasting, pricing, allocation, and decision support |

| Walmart Connect (Retail Media) | Monetization of first-party commerce data | Leverages integrated transaction data to generate higher-margin advertising revenue |

| Drone & InHome Delivery Pilots | Last-mile experimentation | Tests fulfillment speed differentiation and service innovation |

2. Redefining the Role of the Store in a Digital Retail System

Walmart’s transformation reframes the role of its 4,600+ U.S. stores from physical points of sale to distributed nodes in a unified retail intelligence system. Each store now functions as: a same-day fulfillment center, a click-and-collect pickup point, a return processing hub, a last-mile delivery origin, and an in-person experience anchor — while continuing to serve walk-in customers.

This redefinition is the structural enabler of Walmart’s e-commerce growth. By 2024, ~50% of U.S. e-commerce orders were either picked up at or delivered from a Walmart store, not shipped from a warehouse. The physical footprint that was once a competitive vulnerability against Amazon has become a competitive advantage: Walmart is within 10 miles of 90% of the U.S. population.

| New Role of the Store | Walmart Initiatives | Strategic Function |

|---|---|---|

| Experience & Decision Support Hub | Interactive product displays, AI-powered app assistance, associate handheld devices, digital comparison tools | Reduces decision friction, supports high-involvement purchases, and improves conversion through guided engagement |

| Omnichannel Fulfillment Node | Buy Online, Pick Up In-Store (BOPIS); curbside pickup; local delivery; in-store returns for online purchases | Converts geographic density into speed advantage, lowers last-mile costs, and enhances convenience and retention |

| Identity & Data Collection Interface | Mobile app integration; digital receipts; Scan & Go; membership-linked transactions | Connects offline and online behavior into unified customer profiles and strengthens first-party data advantage |

| Operational Intelligence Sensor Network | Inventory sensing technologies; AI demand forecasting; digital shelf labels; centralized analytics dashboards | Improves pricing agility, replenishment accuracy, and coordination efficiency across the store network |

| Monetization & Platform Extension Channel | Walmart Connect retail media; sponsored product placements; in-store digital screens | Expands profit pools beyond product margins, monetizes first-party commerce data, and strengthens ecosystem leverage |

3. Smart Stores as Nodes in the Brand Intelligence System

Walmart has invested heavily in store-level digital infrastructure that connects physical retail to the broader intelligence layer:

- Real-time inventory visibility. Every item in every store is visible to the e-commerce system, enabling accurate online stock displays and BOPIS (buy online, pick up in store) commitments.

- Automated micro-fulfillment. Walmart has deployed robotic micro-fulfillment systems in select stores to automate online order picking, doubling throughput without expanding space.

- Smart shelves and scan-and-go. Digital price tags, computer-vision stock monitoring, and self-checkout via the Walmart app reduce labor cost while improving the in-store experience.

- Connected workforce. Store associates work from Walmart-issued devices that surface task lists, customer requests, and inventory updates in real time.

Each store generates substantial data: traffic patterns, conversion rates, inventory turnover, return reasons, fulfillment SLA compliance. The data flows back to a central intelligence layer where machine-learning models optimize inventory placement, staffing, and pricing across the entire network.

4. Customer Engagement and Competitive Resilience

Walmart’s digital customer-engagement strategy has produced four growth engines:

Walmart+ membership

Launched in 2020, Walmart+ has grown to an estimated 30+ million members. It bundles free shipping (no minimum), in-store discounts, fuel savings, Paramount+ streaming, and other benefits. The program creates lock-in similar to Amazon Prime — high subscriber lifetime value, predictable revenue, and richer behavioral data.

AI-powered personalization

The Walmart app and website use machine-learning models to personalize product recommendations, search rankings, and offer targeting at scale. Walmart processes 240+ million weekly customers and uses behavioral data to drive cross-category sales (e.g., a customer buying baby formula receives diaper recommendations and pediatrician-finder content).

The marketplace

Walmart Marketplace lets third-party sellers list products on Walmart.com. By 2024, the marketplace had grown to hundreds of thousands of sellers and was a meaningful contributor to e-commerce revenue. The marketplace lets Walmart match Amazon’s long-tail product breadth without holding the inventory.

27% e-commerce growth

Walmart U.S. e-commerce growth reached 27% in fiscal 2024 — outpacing Amazon’s U.S. retail growth in the same period. The growth was driven primarily by the store-as-fulfillment-node architecture, not by traditional warehouse-shipped e-commerce.

5. Walmart Connect — Retail Media as a New Profit Engine

Walmart Connect is Walmart’s retail media network — an advertising business that lets consumer brands (PepsiCo, P&G, Unilever, etc.) pay to feature products on Walmart.com, in the Walmart app, on display ads, and increasingly on connected TV (via Walmart’s Vizio acquisition).

By 2024, Walmart Connect was the third-largest retail media network in the U.S. after Amazon and eBay, with growing share. Margins on retail media (50%+) dwarf retail margins (4-6%), meaning Walmart Connect contributes disproportionately to profit even at modest revenue share.

The strategic insight is structural: Walmart’s scale of first-party customer data + its store network as ad inventory creates a retail media position that Amazon must compete with on different terms than it competes with on retail.

6. Beyond Technology: A Shift in Strategic Logic

Walmart’s transformation is not primarily a technology story — it is a logic shift. The traditional retail logic was: own real estate, stock products, serve walk-in customers, optimize unit economics per store. The new logic is: own the customer relationship, use stores as the most efficient fulfillment network, monetize first-party data through retail media, and let the marketplace fill the long tail.

Three implications follow:

- Store footprint = strategic asset. The 4,600+ stores are now Walmart’s most important fulfillment advantage, not its biggest fixed cost.

- Customer data = profit engine. First-party customer data converts into retail-media revenue at margins that exceed retail itself.

- Marketplace = strategic flexibility. The marketplace lets Walmart compete on breadth without the inventory risk.

7. Conclusion: From Asset-Heavy Retailer to Intelligence-Enabled System

Walmart’s 60-year journey from rural discounter to America’s largest retailer has been redrawn into a journey from asset-heavy retail to an intelligence-enabled commerce platform. The transformation has not been quiet: e-commerce growth of 27%, marketplace scale that meaningfully competes with Amazon’s third-party seller business, a retail media network that is now a top-three U.S. player, and a membership program with strong subscriber economics.

For Western brands seeking a reference case in scaling digital transformation across an existing physical footprint, Walmart is the clearest example. The architecture — physical network as fulfillment nodes, first-party data as profit engine, marketplace for long-tail breadth, retail media as high-margin overlay — is reproducible. What Walmart proves is that the Brand Intelligence framework applies as much to a 60-year-old physical retailer as to a digital-native brand — if the intelligence layer is built right.

Cross-References

- Chapter 7: Smart Stores — Walmart’s 4,600+ stores as programmable fulfillment nodes

- Chapter 9: Command Center — cross-store inventory, staffing, and pricing optimization

- Chapter 10: Omni-Domain Marketing — Walmart Connect retail media network

- BI-AR-02: Agentic Commerce — Walmart’s multi-agent deployment (Sparky + Gemini + ChatGPT)

References

Walmart Inc. (2024). Annual Report — e-commerce, Walmart+, Marketplace, and Walmart Connect disclosures.

Reuters (2024). Walmart Vizio acquisition coverage.

eMarketer (2024). U.S. retail media network rankings.

Bloomberg (2024). Walmart Marketplace and third-party seller growth.

Sun, Baohong (2026). Brand Intelligence: Navigating the Transformation in the AI and Web3 Era. Springer Nature.

The Brand Intelligence framework, intelligence-enabled commerce architecture, and related concepts presented in this work are the intellectual property of Baohong Sun, as published in Brand Intelligence (Springer Nature, 2026). License: CC BY-NC-ND 4.0.

Frequently Asked Questions

Quick answers to the questions most readers ask about this piece.

How is Walmart transforming its retail network?

Walmart is converting 4,700 US stores into distributed nodes of a unified retail intelligence system — each store functioning as same-day fulfillment center, click-and-collect pickup, return processing hub, last-mile delivery origin, and experience anchor.

What is Walmart Connect?

Walmart Connect is Walmart's retail-media network, monetizing first-party customer data through sponsored placements, display advertising, and in-store digital screens. It became a top-three US retail-media platform by 2024.

How much of Walmart's e-commerce is fulfilled from stores?

Approximately 50% of US e-commerce orders by 2024 were either picked up at or delivered from a Walmart store, not shipped from a warehouse. Walmart is within 10 miles of 90% of the US population.

What is Walmart's e-commerce growth rate?

27% e-commerce growth (FY2024), driven by store-fulfilled delivery, the third-party marketplace, and Walmart+ membership. The marketplace meaningfully competes with Amazon's third-party seller business.

What is the CDP plus ADC pairing at Walmart?

A Customer Data Platform paired with an Algorithmic Decision Center — the US analog to China's private-domain stack. CDP unifies customer identity across channels; ADC turns customer signals into retail-media, pricing, and assortment decisions in real time.

Download the watermarked PDF

The full case is on this page. The PDF is the formatted, citable version with full references and figures. Enter your email to download the watermarked copy and receive the monthly digest of new cases, articles, and applied research. Unsubscribe anytime.

Subscribe & download PDF →